What counts as a "loan app"

The term covers three different products that share one thing in common: the entire transaction happens inside an iOS or Android app, with no branch visit and usually no paperwork. The three products are personal-loan apps (Upstart, SoFi, LendingClub, Upgrade, OppLoans), cash-advance and earned-wage-access apps (Earnin, Dave, Brigit, MoneyLion Instacash, Chime SpotMe), and credit-builder apps (Self, Kikoff, MoneyLion Credit Builder Plus). Each one underwrites differently, prices differently, and reports differently. Treating them as one category is the most common reason borrowers end up in the wrong product.

Personal-loan apps issue installment loans of $500 to $50,000 over six to 60 months. They run a soft credit pull when you check your rate, then a hard pull when you accept. APRs typically span 7% to 36%, occasionally higher for subprime borrowers. Cash-advance apps do not run a credit check at all. They underwrite by linking to your bank account through Plaid or Finicity and watching your deposit pattern. They lend in two-week chunks of $20 to $500 and pull repayment automatically on payday. Credit-builder apps usually hold the principal in a locked account while you make monthly payments that are reported to the bureaus, so the loan is more about the tradeline than the cash.

How approval really works

For a traditional personal loan, the app reads your FICO score, your debt-to-income ratio, your reported income, and your stated loan purpose. Many lenders also pull alternative data: education, employer, and even payment patterns on subscriptions you hold. A 700 FICO with stable income usually clears in seconds. A 580 FICO can clear too, but at a much higher APR.

For a cash-advance app, the underwriting is mostly about cash flow. The app needs to see at least one consistent direct deposit, an active checking account that does not chronically overdraft, and a positive end-of-day balance pattern. Gig workers and 1099 earners have a harder time here because the deposits are irregular, which is why apps like Giggle Finance built underwriting specifically for that pattern.

How the money actually arrives

Standard ACH funding hits your account in one to three business days and is almost always free. "Instant" or "express" funding moves the same money over a debit-card rail in under thirty minutes and costs $1.99 to $13.99 depending on the app. The cash is the same cash either way. You are paying for impatience.

For installment loans, the deposit usually clears overnight after final approval. Some lenders, including LightStream and SoFi, advertise same-day funding for accepted offers received before a daily cutoff. For app-based products, expect the money to land at the next business day's open if you applied in the evening.

How repayment is pulled

This is the part most first-time borrowers underestimate. Whether it is an installment loan or a cash-advance app, you are signing an ACH authorization that lets the lender debit your checking account on a fixed schedule. For a personal loan, that is one debit per month. For a cash-advance app, the debit lands on your next payday and pulls the full advance plus any expedite fee or tip in a single transaction.

If the balance is not there, the bank can return the debit as NSF (non-sufficient funds) and charge $27 to $35 for the failed pull. Some lenders will retry. The CFPB's Payday Rule (effective March 30, 2025) caps repeat ACH attempts at two before the lender must obtain fresh authorization, but the bureau has indicated it will not prioritize enforcement, so your real protection is your own bank's policies and your right to revoke ACH authorization in writing.

What the credit bureaus see

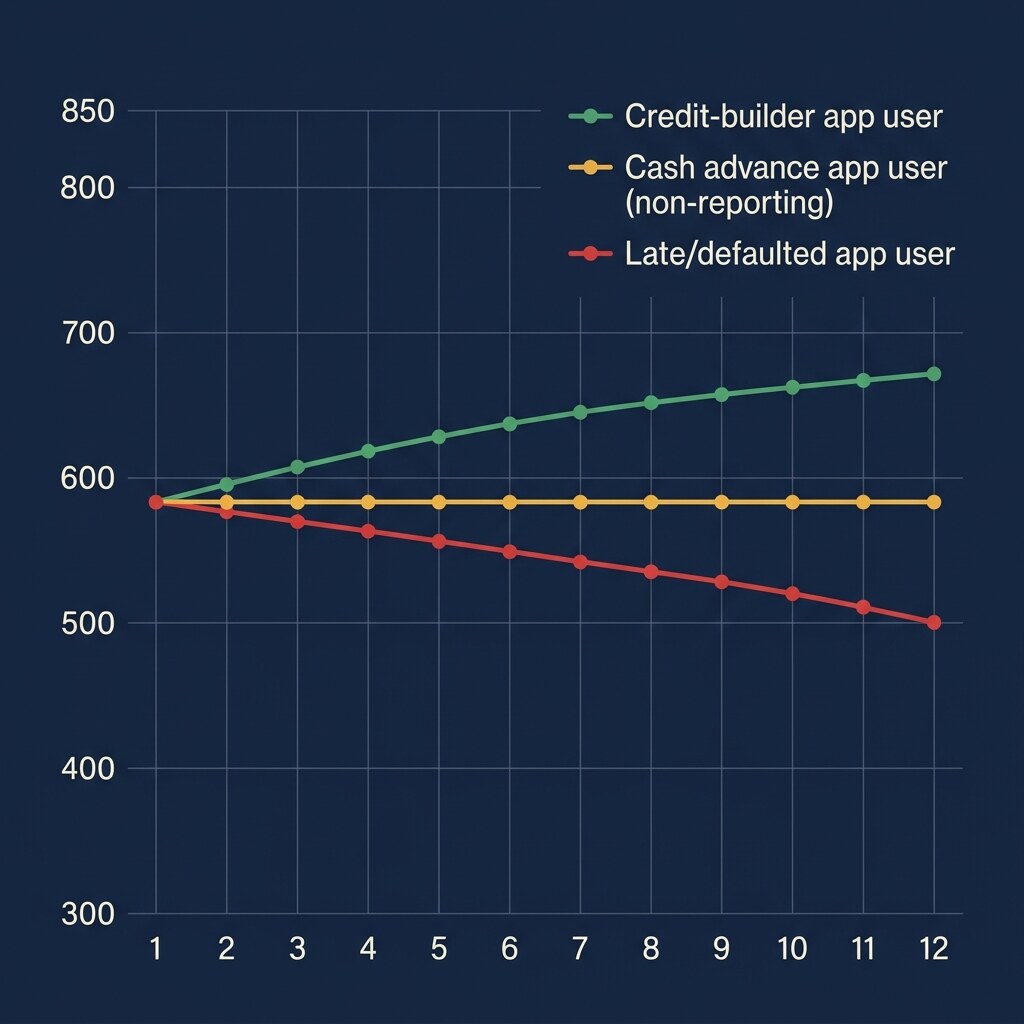

Almost every personal-loan app reports to all three bureaus (Experian, Equifax, TransUnion). On-time payments build your file. Missed payments hit your score within 30 days late and stay on the report for up to seven years. Most cash-advance apps do not report at all, so on-time use does nothing to build credit, but a default that goes to collections can still surface as a third-party tradeline through the back door.

Credit-builder products are the cleanest path from thin file to scorable file. Six to twelve months of on-time payments on Self, Kikoff, or MoneyLion Credit Builder Plus typically adds 30 to 80 FICO points to a brand-new file. The catch is that the cash is locked until the loan ends.

Where to go from here

Pick by job to be done. Need cash this week and have a clean checking account? A cash-advance app is fastest. Trying to consolidate a $4,000 credit-card balance? An installment app like SoFi or Upgrade is cheaper. Trying to repair your file? Start a credit-builder. Read our deeper guides on cash advances vs. payday loans, which apps report to the bureaus, and the true cost of every fee shape before you tap install on anything.