A $300 advance from a loan app can cost you anywhere from $6 to $45 for the same 14-day window, and the product advertising "0% APR" is often the most expensive one. The true cost of loan apps is the sum of every fee the product charges you in a pay period (tip, expedite, subscription, origination, interest) divided by the advance amount, annualized. Anything else is marketing. This piece gives you the normalization math and walks through a $300, 14-day advance across five real apps so you can stop comparing features and start comparing numbers.

Why the Sticker Price Keeps Lying to You

Truth in Lending (Regulation Z, 12 CFR 1026) requires APR disclosure only when a finance charge crosses $5, or $7.50 for loans of $75 or more. Small, repeat advances are engineered to slip under that line. An app can charge you $4.99 to get your $100 today, call it a convenience fee, and never mention APR at all.

The CFPB tried to close that gap. In July 2024 the bureau proposed an interpretive rule that would have treated tips, expedite fees, and required subscription fees as finance charges under TILA. In one of its own examples, a $100 EarnIn advance with an $11 tip and a $4 expedite fee (7-day term) penciled out to a 498% implied APR. That proposal was withdrawn in December 2025. So the old disclosure gap is back, legally blessed, and the responsibility for computing real cost now sits with you.

The Four Fee Shapes You Are Actually Paying

Loan apps do not compete on the lowest price. They compete on which fee is hardest to see. There are four main shapes, and most apps combine two or three.

- APR. The honest one. Stated as a percentage, covers interest and mandatory charges. OppFi installment loans sit at 160 to 195% disclosed APR. Possible Finance runs roughly $10 to $25 per $100 borrowed depending on state, which typically lands at 150 to 180% effective.

- Origination fee. A one-time cut taken off the top, usually 1 to 8% of the loan. You borrow $1,000 with a 5% origination, $950 hits your account, but you owe back $1,000 plus interest.

- Subscription. A flat monthly fee that unlocks the ability to borrow. Brigit Plus charges $9.99 per month. Dave runs $1 to $15 depending on tier. You pay this whether you borrow or not.

- Tip or expedite. The fuzziest one. Tips are framed as optional but the UX often defaults them above zero. Expedite fees (the charge to get cash today instead of in three business days) run $1.00 to $5.99 across the category, averaging $3.18 according to CFPB market data from 2024.

The Formula: Pay-Period Effective APR

Forget what the app screen says. Here is the arithmetic you need.

Total cost = every fee attributable to this advance in this pay period. That includes the prorated share of any monthly subscription you are paying because of this product.

Effective APR = (Total cost / Advance amount) x (365 / Days to repay) x 100.

A $10 cost on a $100 advance repaid in 14 days: (10/100) x (365/14) x 100 = 260.7% APR. That is the number that belongs on the receipt. Nothing about it is hostile math. It is the same formula Regulation Z uses when it is allowed to.

A $300, 14-Day Advance Across Five Real Apps

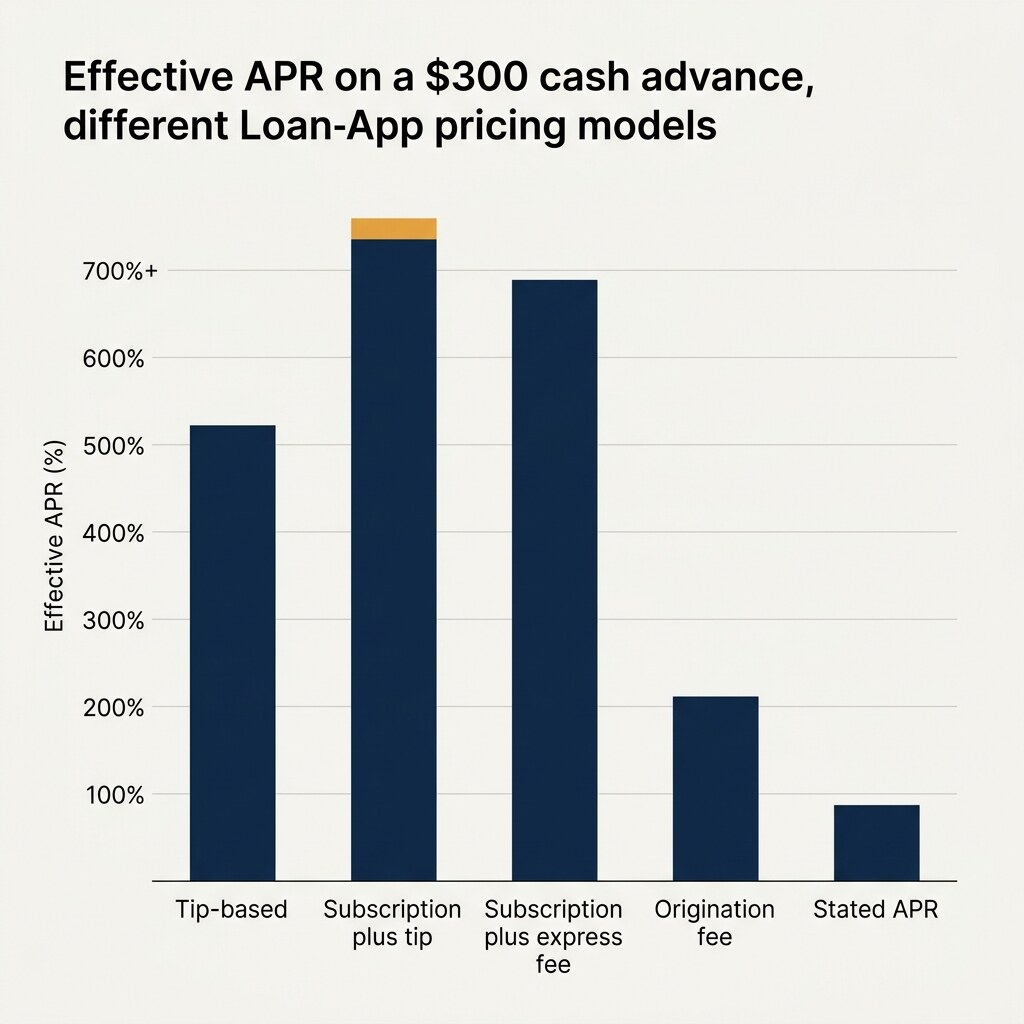

Assume you need $300 today, you will repay in 14 days, and you are paying the expedite fee because waiting three business days defeats the point. Subscriptions are prorated to the 14-day window (half the monthly fee). Tips assumed at the UX default where applicable. Re-verify current pricing before you pull the trigger, because these schedules change quarterly.

| App | Fee Structure (prorated to 14 days) | Total Cost | Effective APR |

|---|---|---|---|

| Dave ExtraCash | $2.50 sub + $3.00 expedite + $6.00 default tip (10%) | $11.50 | ~100% |

| EarnIn Cash Out | $4.99 expedite + $9.00 default tip | $13.99 | ~122% |

| Brigit Plus | $5.00 sub + $1.00 to $6.00 Express | $6 to $11 | 52% to 96% |

| MoneyLion Instacash | $3.99 Turbo + $5.00 optional tip | $8.99 | ~78% |

| Possible Finance | $15 per $100 over 8 installments | $45 | 97% to 180% |

Two things jump out. First, the spread between cheapest and most expensive is almost 8x on the same dollar amount. Second, the app with the highest nominal cost (Possible Finance at $45) is also the only one that reports to the credit bureaus, so the "expensive" label depends on whether you value the credit build at all.

The Tip Problem

Tips are where the disclosure game gets interesting. Federal law, for now, does not treat them as finance charges. State regulators disagree. The Pennsylvania Attorney General's 2024 Assurance of Voluntary Compliance with SoLo Funds, and a parallel action from the DC AG, both established that when a tip is UX-defaulted above zero, it is a finance charge under state consumer protection law. Connecticut's Department of Banking reached the same conclusion.

In plain English: if the app pre-fills a tip and you have to tap through extra screens to set it to zero, it is not really optional. Several federal courts have not ruled on this yet. Your state regulator may already agree with you that you are being charged.

When a Higher APR Is Actually Cheaper

APR is annualized. A 300% APR on a $100, 10-day advance costs you $8.22. A 36% APR on a $3,000, 36-month installment loan costs you $1,905 in interest. The second loan has the lower rate and the much larger total cost.

For a one-time, small, short-duration need (the car won't start, you need $150 to get to work tomorrow), a three-digit APR on a two-week advance can be a rational choice. The math breaks when you roll that advance cycle after cycle. CFPB's 2024 paycheck advance market report found that employer-integrated EWA users took an average of 27 advances per year. At 27 advances with even modest expedite fees, a "free" app costs real money.

A 5-Question Checklist Before You Tap Accept

- What is the total dollar cost of this specific advance, adding every fee the app will charge my account in the next 30 days?

- Am I paying a monthly subscription because of this product? If yes, prorate it to this pay period.

- What is the default tip or donation the UX is suggesting, and can I genuinely set it to zero in one tap?

- When exactly will the auto-debit hit my bank account, and what is my balance forecast for that day?

- Divide total cost by advance amount, multiply by (365 / days to repay), multiply by 100. If that number scares you, close the app.

Where Federal Law Stops and State Law Starts

The CFPB's December 2025 withdrawal of its proposed EWA rule pulled federal APR disclosure requirements back to where they were pre-2024. But state-level enforcement is live. California's DFPI runs an EWA registration regime with fee caps on mandatory charges. New York's 16% civil usury cap has been the basis for New York AG Letitia James's 2025 suit against DailyPay and MoneyLion. The SoLo Funds settlements in PA and DC put tip-default mechanics directly on the enforcement map.

If you live in California, New York, Connecticut, the District of Columbia, or a handful of other states with active consumer-protection offices, the legal definition of "the true cost" in your jurisdiction may already include fees the app swears are optional.

What This Means for Your Checking Account

Loan apps are not getting cheaper. The 2025 withdrawal of federal APR-disclosure pressure means the subscription model and the tip model will spread, not shrink. The only defense is the one nobody ships with the product: arithmetic. Do the pay-period effective APR once, write it down, compare it against the next app on your phone. The cheapest product in the category is routinely 8 to 10 times cheaper than the most expensive one, and the labels on the App Store will not tell you which is which.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Is a loan app subscription fee legally part of the APR?

Under current federal law, no. The CFPB's December 2025 withdrawal of its proposed interpretive rule means subscription fees are not treated as TILA finance charges. State regulators in California, New York, and elsewhere have taken a stricter position on required fees tied to borrowing, but there is no federal mandate to roll subscriptions into disclosed APR.

02 How do I calculate effective APR on a cash advance app?

Add every fee you pay because of the advance (expedite, tip, prorated subscription). Divide that total by the advance amount. Multiply by 365 divided by the number of days until repayment. Multiply by 100. A $10 cost on a $100 advance repaid in 14 days works out to 260.7% effective APR.

03 Why do loan apps advertise 0% APR when I still pay fees?

Regulation Z requires APR disclosure only when a finance charge exceeds $5 (or $7.50 on loans of $75 or more), and tips plus expedite fees are not classified as finance charges under current federal guidance. Apps structure small, fast advances to stay under those thresholds, which lets them state 0% APR while collecting real fees.

04 Are tips on loan apps truly optional?

Legally optional, practically not always. The Pennsylvania and DC Attorneys General settled with SoLo Funds in 2024 on findings that UX-defaulted tips functioned as finance charges under state law. If an app pre-fills a tip amount and requires extra taps to zero it out, you are looking at a design choice regulators in several states treat as a fee.

05 Which loan app fee structure is cheapest for small, occasional borrowing?

For a one-time $100 to $300 advance you repay in two weeks, a pay-per-use product with no subscription (like MoneyLion Instacash with only the Turbo fee) tends to pencil out cheapest. Subscription apps pay off only if you borrow at least two to four times per month, because the fixed monthly fee dilutes across more advances.

Related articles

Best Loan Apps for Gig Workers and the Self-Employed: What Actually Approves You Without W-2s

Are Loan App Subscription Fees Worth It? The Break-Even Math on Brigit, Dave, Tilt, and MoneyLion