Earned wage access (EWA) is not one product. It is two products wearing the same name: employer-integrated EWA, where your company partners with a provider like DailyPay or Payactiv and repayment happens through payroll deduction, and direct-to-consumer EWA, where apps like Earnin, Dave, and Brigit pull from your bank account with no employer involvement. The CFPB's December 23, 2025 Advisory Opinion formally declared "covered" employer-integrated EWA exempt from TILA, while New York's Attorney General was, in the same year, suing DailyPay and MoneyLion for alleged usury. That contradiction is the story, and it determines which EWA you should actually use.

Two Different Products Called the Same Name

More than 7 million US workers accessed roughly $22 billion through paycheck advance products in 2022, and transaction volume jumped over 90% from 2021 to 2022, per the CFPB's July 2024 market report (the US GAO's independent EWA report reaches similar conclusions). Most of those workers could not tell you whether their app was integrated with their employer's payroll system or simply monitoring their checking account. The distinction matters. It drives cost, repayment mechanics, credit reporting, and which federal and state rules apply.

Here is the split in one sentence: employer-integrated EWA is paid back by your employer out of your next paycheck before the net deposit ever reaches you, and direct-to-consumer EWA is paid back by an ACH pull from your bank account on a date the app chooses.

How Employer-Integrated EWA Actually Works

Your employer contracts with a provider. DailyPay covers roughly 6 million employees across 1,200+ employers and ties into 180+ HCM and payroll systems. Payactiv plugs into ADP, Paychex, Kronos, and 70+ others. Branch runs a wallet model with Evolve Bank and Lead Bank and earns its money on interchange rather than employee fees.

When you pull an advance, the provider front-funds it. On payday, the employer deducts the advanced amount (plus any expedite fee you chose) from your gross pay before the direct deposit runs. You never owe the provider directly. If you leave the job, there is no balance to collect, because the product by design cannot advance money you have not already earned.

CFPB market data from 2024 shows 92.5% of fee revenue on employer-partnered products comes from expedited-transfer fees, typically $1.00 to $5.99 and averaging $3.18. Standard ACH (1 to 3 business days) is free on Payactiv, Branch, and most employer-partnered DailyPay instances.

How Direct-to-Consumer EWA Actually Works

There is no employer on the other side. You connect Earnin, Dave, or Brigit to your checking account. The app watches your deposits, infers whether you are getting paid, and decides how much it will front you. On a date the app picks (often your next payday), it runs an ACH debit against your account.

Two consequences follow. First, the product is priced on top of a checking-account risk model, not a payroll-deduction guarantee, which is why D2C apps stack expedite fees, tips, and subscriptions where employer-integrated products typically do not. Second, if you switch banks, overdraft, or the deposit the app was counting on shows up late, the debit can hit a $0 balance and trigger NSF fees at your bank on top of whatever the app charges for failed collection (the same overdraft cascade we walk through in cash advance apps vs. payday loans).

| Product | Employer Integrated | Funding Source | Fee Model | Max Advance | Credit Check | Collections |

|---|---|---|---|---|---|---|

| DailyPay | Yes | Payroll deduction | Expedite fee $1.99 to $3.49 | Up to 100% of earned wages (employer cap) | No | No |

| Payactiv | Yes | Payroll deduction | Free standard, expedite optional | Per employer policy | No | No |

| Branch | Yes | Wallet + payroll | Free to employer and employee | Up to 50% of earned wages | No | No |

| Earnin | No | Bank account debit | Optional tip + expedite | $100 to $750 | No | Yes, via ACH |

| Dave ExtraCash | No | Bank account debit | Subscription + 5% fee | Up to $500 | No | Yes, via ACH |

The Cost Picture: Who Pays, and How Much

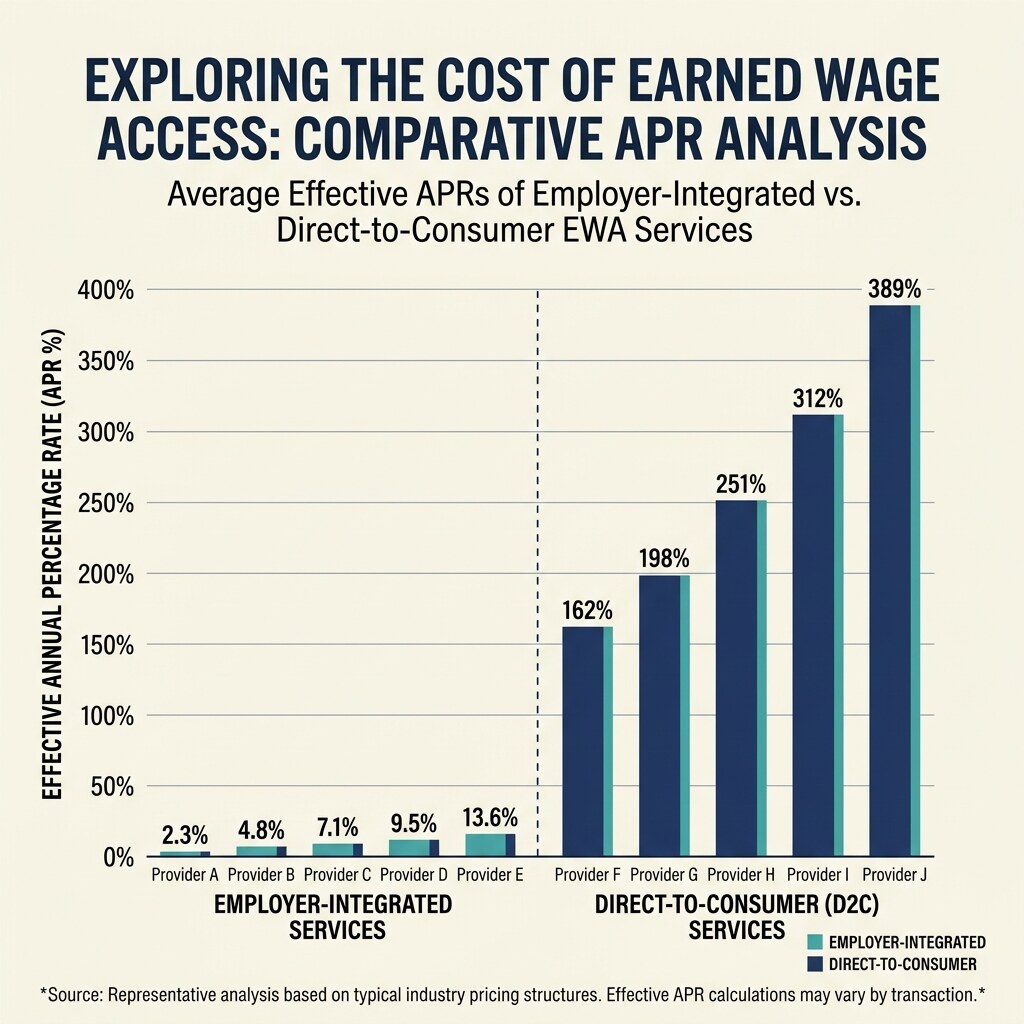

The CFPB's 2024 market report found the average blended effective APR on employer-partnered EWA advances was 109.5%, with workers taking an average of 27 advances per year. That number is high, and it should be. It reflects a product that is often "free" on standard ACH and cheap on expedite, used repeatedly.

D2C apps run higher. The same CFPB work, looking at an example $100 EarnIn advance with an $11 tip and a $4 expedite fee over seven days, implied a 498% APR. Dave's February 2025 transition to a 5% flat advance fee on top of its $1 to $15 monthly subscription shifted its pricing architecture but not its effective APR, which still lands in triple digits for small, fast advances.

The December 2025 CFPB Advisory Opinion

On December 23, 2025 the CFPB published an Advisory Opinion declaring that "covered" EWA is not credit under TILA or Regulation Z. To qualify as covered, a product must meet four tests: it cannot exceed earned wages, it must use payroll deduction through an employer, the provider must represent in writing that it has no legal claim for non-repayment and will not furnish to credit bureaus, and it cannot assess credit risk. The same action rescinded the July 2024 proposed interpretive rule that would have pulled tips, expedite fees, and subscriptions into the TILA finance-charge definition.

Practical translation: DailyPay, Payactiv, and Branch, operated as employer-integrated products with the four hallmarks above, sit outside federal lending law. Earnin, Dave, Brigit, and MoneyLion Instacash, which monitor bank accounts and collect via ACH, do not automatically qualify as "covered" and remain on contested legal ground.

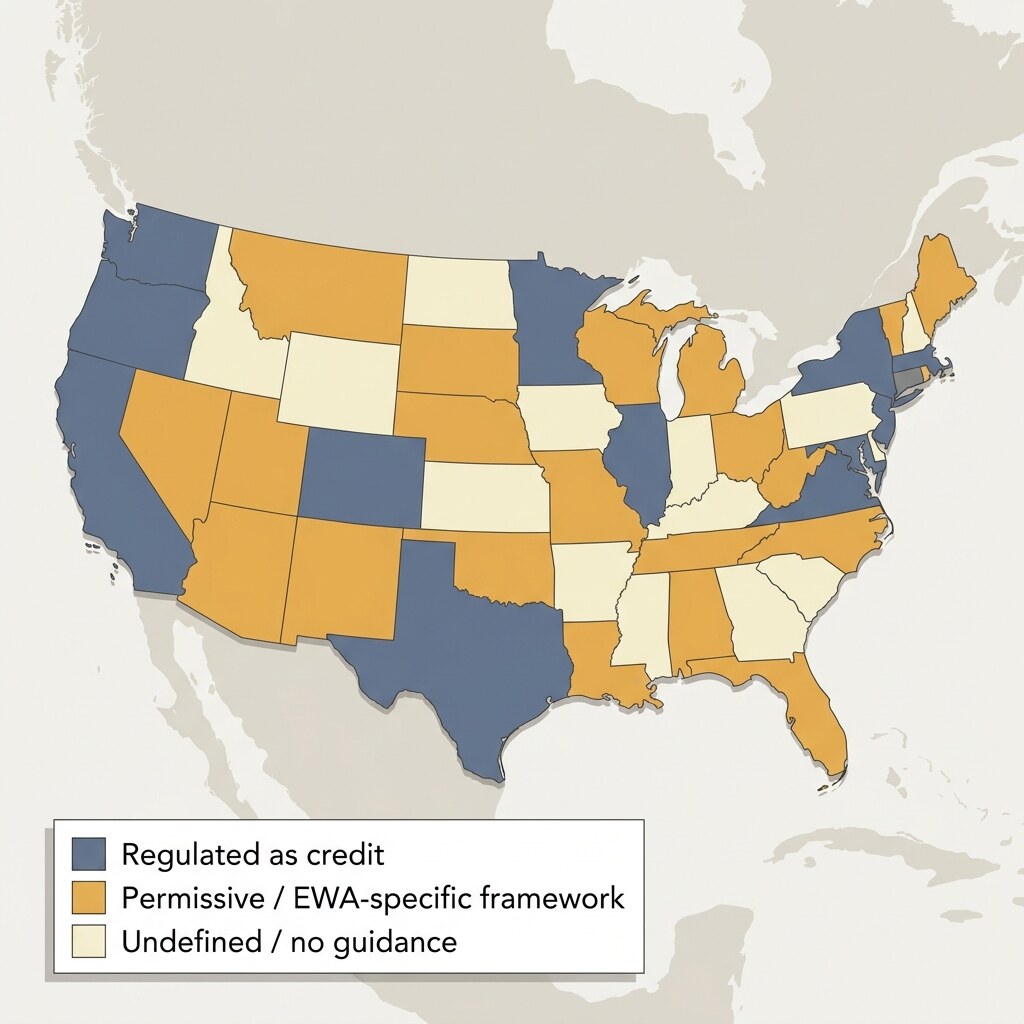

The State-Level Map

Federal clarity does not equal state clarity. A cluster of states has written EWA statutes classifying covered products as non-loans, generally requiring registration and an annual fee in the $1,000 range:

- Nevada (SB 290, effective July 2024)

- Missouri (effective 2023)

- Kansas (effective July 2024)

- Wisconsin, South Carolina, Arkansas

- Utah (2025)

- Connecticut and Louisiana (2025 enactments)

The contested side of the map is smaller but louder. California's DFPI, under its EWA registration regime effective February 15, 2025, treats certain "tips" as charges subject to fee caps (we go deeper on tip economics in tip-based loan apps: the true cost). New York Attorney General Letitia James filed suit in April 2025 against DailyPay and MoneyLion, alleging that the effective rates on their products (in some cases up to 750% per the complaint) violate New York's 16% civil usury cap. A parallel FTC action against Dave is pending on deceptive tip and fee practices.

Two regulators, one product type, opposite conclusions. That is where EWA sits in 2026.

When EWA Beats a Loan App, and When It Doesn't

Employer-integrated EWA, used once or twice a pay period on standard ACH, is one of the cheapest ways in the consumer-credit system to smooth a cash flow gap. There is no interest, no collection risk against your checking account, and no credit-bureau footprint.

It stops being cheap when you run it 27 times a year, always on expedite, always in small amounts. At that frequency the expedite fees stack into three-digit effective APRs and you are paying real money to solve a structural income problem an advance cannot fix.

D2C EWA makes sense when your employer does not offer an integrated product, you need $100 to $500 before your next deposit, and you will genuinely use the product once. It stops making sense when the subscription fee becomes a recurring charge you forget about, or when the UX-defaulted tip pushes the real cost into payday-loan territory.

How to Tell Which Kind of EWA You Are Actually Using

- Did your employer tell you about the app through HR or onboarding? If yes, it is likely employer-integrated.

- Does the app ask for your bank login (Plaid, Finicity, MX)? If yes, it is almost certainly direct-to-consumer.

- When you take an advance, where does the repayment come from? Payroll deduction before net pay means employer-integrated. ACH debit from your checking account means D2C.

- Does the app ask about tips or offer a subscription tier? Strong D2C signal.

- Can you access the app after you leave the job? If yes, D2C. If the account goes dark, employer-integrated.

Hybrid Products and the Gray Zone

Not everything fits cleanly. MoneyLion Instacash advertises integration with some employers but primarily operates on bank-account monitoring. Payactiv layers optional premium features on top of its employer-partnered core. Branch blurs the line further with its wallet architecture. The December 2025 CFPB four-prong test is the cleanest way to place a product: if it uses payroll deduction, caps at earned wages, disclaims collection rights, and does not assess credit, it is covered EWA. If it fails any prong, it is something else, and you should price it accordingly.

What This Means for Your Paycheck

Federal law now treats the two EWA models very differently. Consumer experience does not. The same worker can have DailyPay through their employer and Earnin on their phone and have no idea the products are structurally opposite. The cheap product is the one that does not need to collect from your checking account. That is almost always the employer-integrated one, when it is available. The rest of the category deserves the same scrutiny you would give a payday loan, because in New York, California, and a growing list of states, that is how regulators are starting to treat it.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Is earned wage access a loan?

Under the CFPB's December 23, 2025 Advisory Opinion, "covered" EWA (payroll-deducted, capped at earned wages, no collections, no credit check) is not credit under TILA. New York's Attorney General disputes this for some products and has sued DailyPay and MoneyLion alleging usury. The federal answer is no; state answers vary.

02 What is the difference between DailyPay and Earnin?

DailyPay is employer-integrated: your company contracts with DailyPay and repayment comes out of your paycheck through payroll deduction. Earnin is direct-to-consumer: you connect your bank account, it monitors deposits, and it debits you via ACH. DailyPay cannot collect from your checking account. Earnin can.

03 How much does earned wage access cost on average?

CFPB data from 2024 put the average blended effective APR on employer-partnered EWA at 109.5%, with the average user taking 27 advances per year. Expedite fees drive 92.5% of fee revenue and typically run $1.00 to $5.99, averaging $3.18. Direct-to-consumer products often price higher when tips and subscriptions are included.

04 Does earned wage access affect my credit score?

Covered employer-integrated EWA products do not report to credit bureaus and cannot legally pursue collections, per the CFPB Advisory Opinion definition. That means no positive or negative credit impact from on-time use or missed repayment. Direct-to-consumer apps vary; most do not furnish to bureaus either, but failed ACH debits can trigger bank overdraft fees that indirectly affect your financial standing.

05 Which EWA apps are available in California and New York?

California's DFPI EWA registration regime became effective February 15, 2025; only registered providers can legally operate, and several apps withdrew or restructured. New York's AG sued DailyPay and MoneyLion in April 2025 alleging usury, and the litigation is pending. Check each app's in-state availability directly, because the list is moving quarter to quarter.

Related articles

Are Loan App Subscription Fees Worth It? The Break-Even Math on Brigit, Dave, Tilt, and MoneyLion

Best Loan Apps for Gig Workers and the Self-Employed: What Actually Approves You Without W-2s