Two products with the same name

"Cash advance" and "earned wage access" get used interchangeably, but legally and structurally they are two different products. A direct-to-consumer cash-advance app (Earnin, Dave, Brigit, MoneyLion Instacash) connects to your personal checking account and debits itself on payday. An employer-integrated EWA product (DailyPay, Payactiv, Branch) is wired into your employer's payroll system and is paid back by your employer out of your next paycheck before the deposit ever reaches you. The CFPB's December 23, 2025 Advisory Opinion drew a hard line: covered employer-integrated EWA is not credit under TILA, while direct-to-consumer apps remain on contested ground that varies state-by-state.

The five fee shapes you will actually meet

Every major app maps to one of five fee structures. The marketing rarely tells you which one you are dealing with, so here is the field guide.

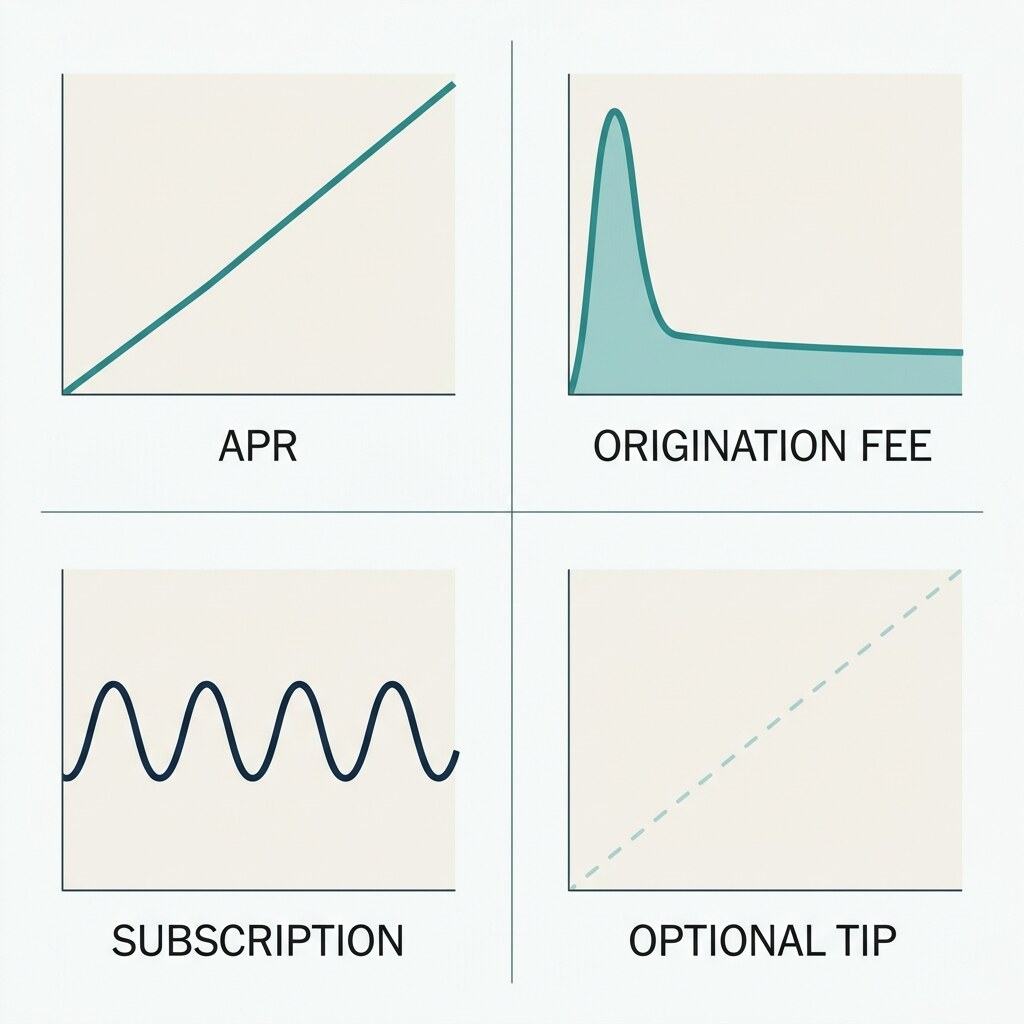

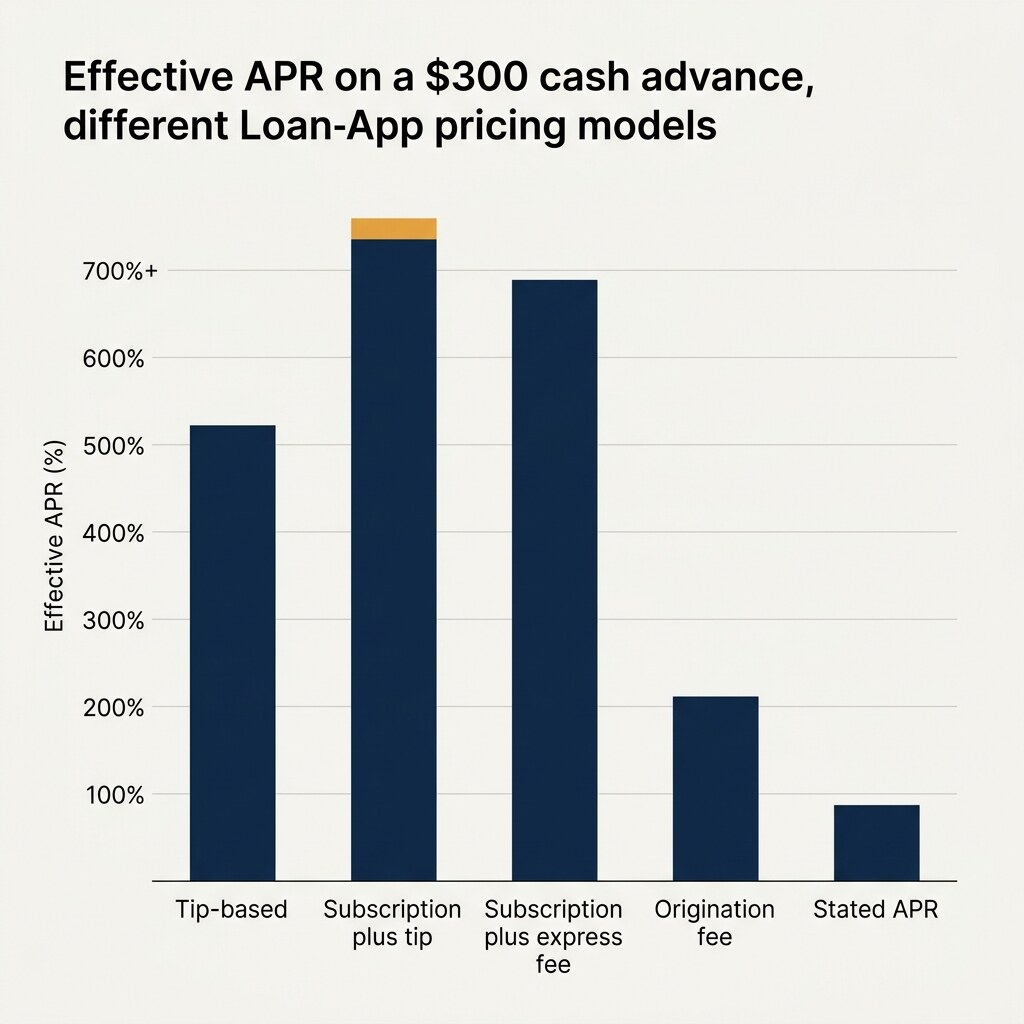

1. Tip plus expedite fee. Earnin is the archetype. The advance is "free." You pay $3.99 to $5.99 to get the cash in minutes instead of days, and the UI prompts you for an "optional" tip the California DFPI found is actually paid 73% of the time. A $100 advance with a $3 tip and a $3.99 expedite fee, repaid in 14 days, lands at roughly 182% effective APR.

2. Monthly subscription. Brigit charges $9.99 (Plus) or $14.99 (Premium) per month for advances of up to $250. Whether the subscription pays off depends entirely on how often you borrow that month. One advance and the per-advance cost is the entire $9.99. Four advances and it is $2.50 each. The math rewards heavy use, which is an unusual incentive for a credit product.

3. Flat percentage. Dave moved to this in February 2025 after the FTC sued the previous tip-based version: 5% of the advance with a $5 minimum, $15 cap, plus a $1.99 to $13.99 express fee. The most honest pricing structure in the category and the result of federal enforcement pressure.

4. Tip-default with subscription. MoneyLion Instacash stacks a Turbo delivery fee with optional tips and an upgrade-to-RoarMoney bundle. The New York Attorney General sued MoneyLion and DailyPay in April 2025 alleging effective rates "frequently up to 750%" once tips and fees stacked.

5. Genuinely free, with conditions. Chime SpotMe charges no fees and does not solicit tips for qualifying users. The catch is "qualifying": you need a Chime checking account with a recurring direct deposit. SpotMe is subsidized by debit-card interchange, not by the borrower.

The break-even number you should know

For a one-time, small, two-week borrow, the cheapest product is almost always a no-tip cash-advance app on standard ACH (Earnin or MoneyLion at $3.99 with no tip). For two-or-more borrows in the same month, a subscription app starts to win on per-advance cost. For larger principals over a longer window ($300 to $500 over two weeks), flat-percentage apps like Dave compress most cleanly because the fee is bounded.

The number that matters more than the marketing label is effective APR: (total fees / advance amount) x (365 / days to repay) x 100. A $5 fee on a $100, 7-day advance is a 261% APR. A $5 fee on a $500, 14-day advance is a 26% APR. Same five dollars, very different products.

The bank-account risk you cannot ignore

Direct-to-consumer apps debit your checking account on payday. If your paycheck lands a few hours late, or if a second app is debiting on the same day, the pull can hit a $0 balance and trigger a $35 overdraft fee at your bank, then a cascading series of fees on every auto-payment that follows. CFPB data from 2024 put US overdraft and NSF revenue at $12.1 billion, with 79% of that paid by 9% of consumers. If you are in that 9%, a "free" cash-advance app is not free; it is an overdraft trigger with a friendlier interface. Employer-integrated EWA does not have this risk because repayment is taken out of your gross pay before net deposit.

Where to dig in next

Read our line-by-line break-even on subscriptions in are loan-app subscription fees worth it, the full federal-state regulatory split in employer vs. direct-to-consumer EWA, and the side-by-side bank-account mechanics in cash advance apps vs. payday loans.