Texas caps contractual interest at 10% per year under Article 16, Section 11 of the state constitution, and Texas borrowers routinely sign loan-app contracts with all-in APRs above 500%, because a separate state licensing structure called the Credit Access Business (CAB) lets a broker charge uncapped fees on top of that 10% interest. If you have ever opened a Texas loan-app contract, seen "10% interest" in one box and "589% APR" in another, and assumed one of those numbers was a typo, neither is. Both are legal. This guide explains why.

Why Texas Has a 10% Cap and 500% APRs at the Same Time

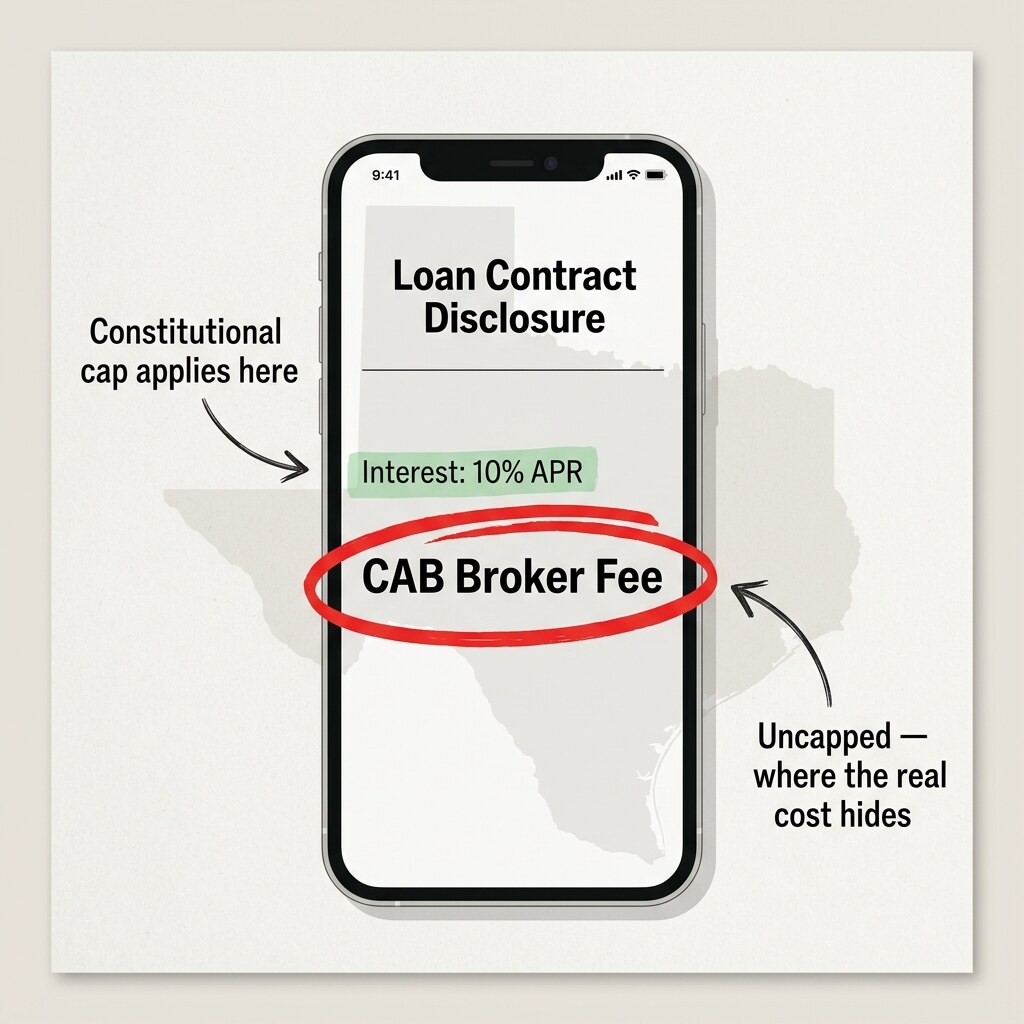

Start with the constitution. Article 16, Section 11 of the Texas Constitution sets the default maximum contractual interest rate at 10% per year absent a legislative carve-out. That single sentence should have ended high-cost lending in Texas. It did not.

Two statutes did the work around it. The Texas Finance Code Chapter 302 covers the base 10% nominal usury cap, Chapter 342 governs "Regulated Lenders," true consumer installment lenders whose interest rate and fee authority is spelled out directly in statute. Chapter 393 governs Credit Services Organizations, a category that, beginning in 2011, expanded into what Texans now know as Credit Access Businesses.

Here is the structure in plain language. The CAB does not lend you money. It arranges a loan for you from a third-party lender. The third-party lender charges 10% interest, obeying the constitution. The CAB charges you a broker fee for the arrangement, and Chapter 393 does not cap that fee. Stack the two and you get an all-in APR that the Texas Office of Consumer Credit Commissioner (OCCC) has reported at roughly 537% for single-payment payday products and 488% for installment payday products in recent annual data cycles.

What a CAB (Credit Access Business) Actually Is

A CAB is a licensee under Chapter 393. To operate, a CAB must:

- Hold an active license from OCCC, searchable in the ALECS system

- File a fee schedule with the state

- Disclose the OCCC toll-free complaint line to every borrower before closing

- Refrain from charging a prepayment penalty

- Comply with local ordinances where they exist (more on that below)

Crucially, the CAB is the entity you deal with inside the loan app. It markets, underwrites, and services. The unaffiliated third-party lender is often invisible to you, and that is the point. The structure exists because it keeps the 10% interest number and the broker fee number on legally separate lines of the contract.

How to Read a Texas CAB Disclosure (Worked Example)

Open a Texas CAB loan disclosure and you will see something close to this on a $500 single-payment loan with a 14-day term:

| Line Item | Amount |

|---|---|

| Amount financed (principal) | $500.00 |

| Interest at 10% annualized for 14 days | $1.92 |

| CAB fee | $100.00 |

| Total of payments | $601.92 |

| Disclosed APR (all-in) | Roughly 530% |

The 10% interest line is almost decorative. The CAB fee is the product. When the fee dwarfs the interest line by two orders of magnitude, that is the CAB model working as designed. Nothing is hidden; the disclosure is all right there. What the disclosure does not say is that in most other states, a fee this size would itself be counted as interest and would run headfirst into a usury cap.

Loan Apps Operating in Texas as CABs

These apps run a CAB-structured product for Texas residents. APR disclosures will typically land between 400% and 600% depending on term and product type:

- CashNetUSA (Enova) - Texas CAB; installment and line-of-credit products inside the app

- Advance Financial - Texas CAB; mobile app plus storefront

- ACE Cash Express - Texas CAB; app plus stores

- Check 'n Go - CAB-arranged products in Texas

- Advance America - Texas CSO/CAB

App Store and Google Play ratings on these apps are higher than the pricing would suggest, typically in the 4.5 to 4.7 range. Borrowers rate the speed and convenience. The price shows up in the disclosure box, not the star count.

Loan Apps Operating in Texas Without the CAB Structure

These apps lend to Texas residents under Chapter 342 (Regulated Lender) licenses or through bank-partner structures that price well below CAB math:

- Possible Finance - Licensed under Texas Finance Code Chapter 342

- Upstart, LendingClub, SoFi, Upgrade - National personal loan apps; credit-tiered APRs below state usury concerns

- OppLoans (OppFi) - Operates in Texas at high APR (160% to 195%), typically outside the CAB structure

- Earnin, Dave, MoneyLion, Brigit - Subscription or tip-based earned wage and cash advance apps available to Texas residents

If you have the credit to qualify for Upstart or SoFi, you are not the target market for a CAB product, and using one is almost always the wrong call. If you do not, the comparison to make is between a CAB product and a Chapter 342 Regulated Lender like Possible Finance, not between two CAB products. (For thin-file alternatives, see loan apps for bad credit under 580 FICO.)

Apps That Decline Texas Residents

A handful of apps either geofence Texas or limit the product. These tend to cluster among tribal-affiliated installment lenders and state-specific earned wage products. Reasons vary. Some do not want to carry CAB licensing. Some lost access to the Texas market after OCCC enforcement actions. If an app declines you at the Texas address step, it is rarely about your credit; it is about their licensing posture.

City-Level Rules in Dallas, Houston, Austin, San Antonio, El Paso

This is the piece most statewide articles skip. Several Texas cities have passed their own payday and auto-title ordinances. Where they exist, they generally limit:

- Cash advance size as a percentage of monthly income (commonly 20% for single-payment and limited by number of installments)

- Number of rollovers or refinances (often three, then full payoff)

- Required principal reduction per installment

Cities with notable ordinances include Austin, Dallas, Houston, San Antonio, and El Paso. A CAB operating in one of these cities must comply with the ordinance on top of state law, and a loan-app disclosure that ignores city rules is a red flag.

Filing a Complaint With OCCC

If you believe a Texas CAB charged a fee the license did not authorize, failed to disclose the CAB fee schedule, charged a prepayment penalty, or misrepresented the product, file with the Office of Consumer Credit Commissioner. What to include:

- Your full loan agreement and any amendments

- The app's disclosure screen at the time of signing (screenshot if possible)

- A clear timeline of payments and communications

- The CAB's name and license number (look it up in ALECS)

Active-duty servicemembers and covered dependents have an additional layer of protection: the federal Military Lending Act caps APR at 36% all-in (MAPR) and preempts the CAB fee structure for covered borrowers. If a CAB product priced you above 36% MAPR while you were covered, file a parallel complaint with the CFPB.

Safer Alternatives Before You Tap a CAB Product

Before you agree to a 500%+ APR product, exhaust the cheaper options. Most Texans who end up in CAB loans have at least one of the following available to them and did not know it:

- Credit union PAL II loans. Federal credit unions can offer Payday Alternative Loans up to $2,000 with 28% max APR and terms up to 12 months. Membership rules vary; Texas has dozens of eligible credit unions.

- Chapter 342 Regulated Lender installment loans. Still expensive at the subprime tier, but cheaper than any CAB by a wide margin.

- Employer-sponsored earned wage access. If your employer offers DailyPay, Payactiv, or Branch, your advance cost is usually a flat fee that is not in the same universe as a CAB APR.

- Nonprofit emergency assistance. Texas utility companies, county community action agencies, and 2-1-1 Texas can route you to short-term hardship funds that do not involve borrowing at all.

Your Next Steps if You're Borrowing in Texas

Three things to do before you sign inside any Texas loan app. Verify the lender or CAB in ALECS by name. Read the disclosure box and total the interest line plus the CAB fee; that total, annualized, is your real APR. If the total is above 36% and you are on active duty or a covered dependent, the loan is likely unlawful under the Military Lending Act and you should stop. Screenshots beat memory; capture the disclosure before you tap "accept."

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Why are Texas loan-app APRs so high if the state caps interest at 10%?

The Texas Constitution caps contractual interest at 10%, but Finance Code Chapter 393 lets Credit Access Businesses charge uncapped broker fees on top of that interest. The third-party lender collects 10% interest, the CAB collects the fee, and the combined APR often lands between 400% and 600%. Both lines appear on your contract because both are legal under Texas law.

02 What is a Credit Access Business in Texas?

A Credit Access Business is a broker licensed under Texas Finance Code Chapter 393 that arranges consumer loans from a third-party lender in exchange for a fee. OCCC issues CAB licenses and publishes them in ALECS. CABs must disclose a fee schedule, provide the OCCC complaint line, and cannot charge prepayment penalties, but the fee itself is not statutorily capped.

03 Are OppLoans and CashNetUSA legal in Texas?

Yes. CashNetUSA operates in Texas under a CAB structure with APRs typically in the 400% to 600% range. OppLoans (OppFi) lends to Texas residents at APRs in the 160% to 195% range, generally outside the CAB structure. Both products comply with Texas law, but their pricing would violate consumer lending caps in many other states.

04 Does the Military Lending Act override the CAB structure?

Yes. For active-duty servicemembers and their covered dependents, the federal Military Lending Act caps all-in APR (Military APR or MAPR) at 36% and preempts state structures that would allow higher rates. A CAB product priced above 36% MAPR to a covered borrower is unlawful. File complaints with OCCC and the CFPB if this happens to you.

05 How do I file a complaint against a Texas loan app?

File online with the Texas Office of Consumer Credit Commissioner at occc.texas.gov/consumers/file-a-complaint. Include your loan agreement, the in-app disclosure screen, a payment timeline, and the CAB's license number from ALECS. OCCC reviews complaints on fee disclosures, license status, prepayment penalties, and deceptive practices, and coordinates with the Texas Attorney General when appropriate.

Related articles

Loan Apps in California: What the 36% APR Cap Actually Means for Your Next Download

Loan Apps in New York: How the 16% Civil and 25% Criminal Usury Caps Shape What You Can Actually Borrow