New York caps non-bank consumer loans at 16% per year civilly and 25% per year criminally, and those two numbers, set in General Obligations Law 5-501 and Penal Law 190.40, are the real reason so many loan apps either reject you at a Bronx zip code or silently disappear from your App Store search in Brooklyn. If you have ever applied on an app that works fine for a friend in New Jersey and been told "not available in your state," you have just met New York's usury regime.

The Short Answer: Why New York's App Options Look Smaller

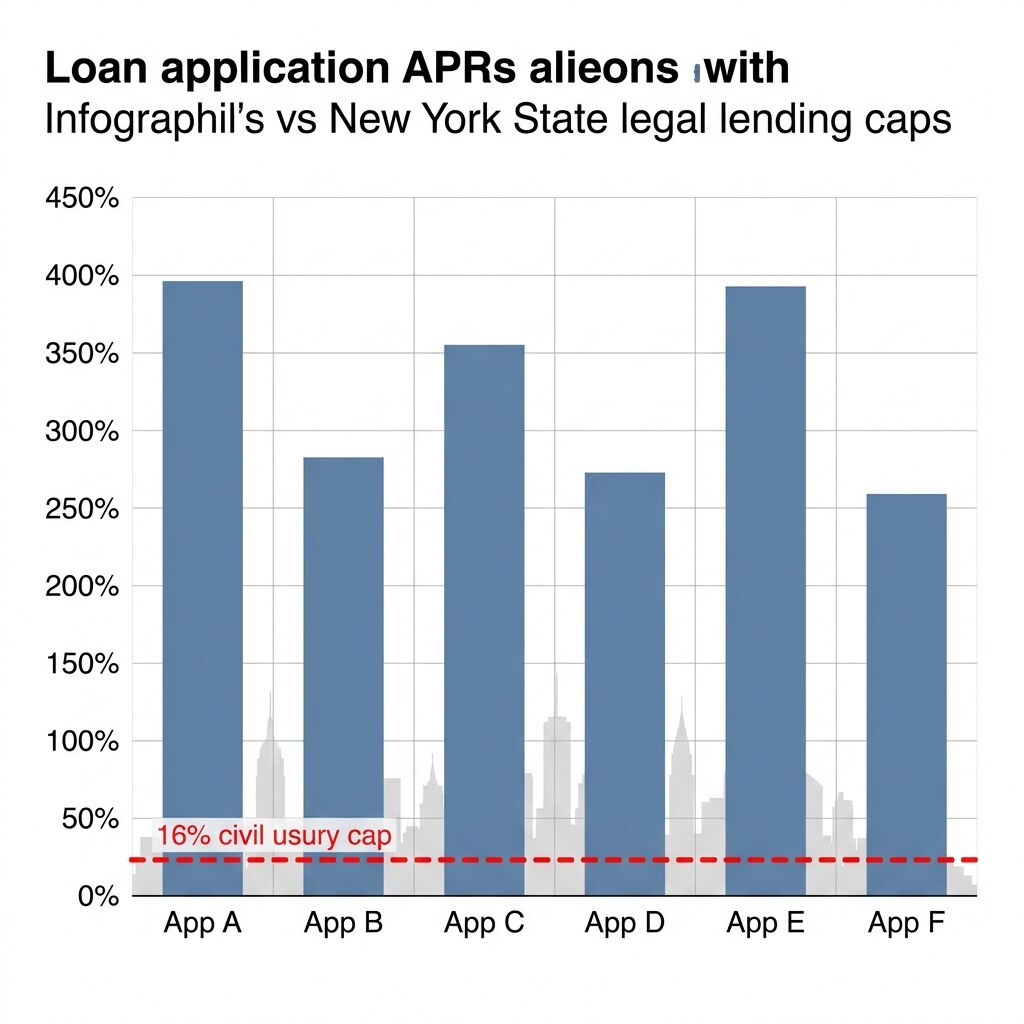

Most "best loan apps" roundups you find online assume a regulatory baseline that does not exist in New York. Outside New York, states often allow non-bank consumer loans at 35% to 36% APR, or far higher under workaround structures like Texas's Credit Access Business model. In New York, the civil cap for loans to individuals under $250,000 sits at 16%, and charging above 25% crosses into criminal usury, a Class E felony under Penal Law 190.40.

Add aggressive enforcement from the New York State Department of Financial Services and a public "true lender" position the department staked out in 2020, and most app-based products priced above 25% APR simply cannot operate here. That is the whole story in one paragraph. The rest of this piece is the fine print.

16% Civil vs. 25% Criminal: What Each Cap Means for You

Civil usury (GOL 5-501): Any non-bank loan to an individual at an annual rate above 16% is civilly usurious. Under GOL 5-511, a usurious loan can be declared void, meaning the borrower may not have to repay the interest, and in some cases not even the principal.

Criminal usury (Penal Law 190.40 and 190.42): Charging above 25% per year without proper authorization is second-degree criminal usury, a Class E felony. If the lender has a prior usury conviction, or if the loan is part of an unlawful debt-collection scheme, the charge escalates to first-degree criminal usury, a Class C felony.

For you as a borrower, the practical consequences look like this:

- A loan priced above 25% APR to a New York resident is presumptively illegal if made by a non-bank lender without federal preemption

- Licensed lenders under Banking Law Article 9 operate within these caps; unlicensed lending is a separate violation on top of any usury claim

- If you were charged above the cap, you may have a defense against collection and, potentially, a claim for restitution

Who Enforces It: NYDFS, the NY AG, and NYC's DCWP

Three agencies matter when you are dealing with a loan app in New York.

The New York State Department of Financial Services licenses most consumer lenders, runs the Licensed Lender program under Banking Law Article 9, and handles the bulk of online-lending enforcement. NYDFS is also the agency that, in a September 2020 public comment, formally opposed the OCC's proposed "true lender" rule, warning that the rule would let non-bank fintechs use bank partners to export triple-digit APRs into New York. That position has shaped which bank-partner apps are willing to operate in the state.

The New York Attorney General brings deceptive-practices actions and has historically coordinated with other state AGs on multi-state settlements against small-dollar lenders.

In New York City, the Department of Consumer and Worker Protection (DCWP) takes complaints on debt collection and deceptive lending aimed at residents of the five boroughs. If you live in NYC and your issue involves collection practices on top of pricing, DCWP is a useful parallel filing.

The 2020 "True Lender" Position and Why It Matters for Bank-Partner Apps

Here is the trick many loan apps use to dodge state caps: partner with a federally chartered or FDIC-insured bank in a permissive state, have the bank originate the loan on paper, then assign the loan to the fintech to service. The bank's charter, the theory goes, lets the loan travel across state lines at the bank's rate, not the borrower's state rate.

NYDFS disagrees. The department's public stance, articulated in its 2020 comment letter, is that when a non-bank platform does the marketing, underwriting, funding, and servicing, the platform is the true lender and New York law applies. That is why OppLoans, NetCredit, CashNetUSA, and most tribal-affiliated installment products do not originate consumer loans to New York residents, even though they operate freely in Texas and Utah.

Apps That Generally Work for New York Residents

The apps below operate in New York in some form, though several run a different product here than they do in other states. Verify current availability in the app before you apply; New York status changes more often than most borrowers realize.

- Dave (ExtraCash): Subscription model with small-dollar advances. Dave avoids traditional interest charges and relies on membership and optional "tips." Works in New York.

- EarnIn: Base earned wage access product (no mandatory fee) is available to New York users whose employers are supported. In CFPB comment letters, EarnIn acknowledged that a $100 advance with a typical tip plus expedite fee implies an APR near 498% if you apply finance-charge accounting, which is exactly why tip-based EWA is under regulatory scrutiny nationally.

- Brigit: Subscription-based advances tied to plan tier. Operates in New York.

- MoneyLion Instacash: Available in New York with product constraints around the RoarMoney account.

- Chime SpotMe: Not a loan; it is fee-free overdraft tied to a Chime account. Works in New York.

- Upstart, SoFi, LendingClub, Upgrade: National personal loan apps that price under 25% and operate through licensed structures. Available to prime and near-prime New York borrowers.

App Store and Google Play ratings for these apps cluster between 4.5 and 4.8 stars at time of writing. Star ratings do not tell you anything about whether the app's New York product is priced differently from its national version, which is the question that actually matters for your wallet.

Apps That Do Not Work in New York

If you have seen any of the following advertised and wondered why you cannot get approved, this is why:

- OppLoans / OppFi: Personal loans typically priced at 160% to 195% APR. Outside anything New York allows via a non-bank channel. OppFi does not originate consumer loans to New York residents.

- NetCredit, CashNetUSA, Check 'n Go: Installment and line-of-credit products priced above the civil cap. Geofenced out of New York.

- Most tribal-affiliated installment apps: These claim sovereign-lender status. NYDFS and the NY AG have challenged that position aggressively over the last decade.

- SoLo Funds: The peer-to-peer "tip" lender has faced actions from the DC AG, the CT Department of Banking (2023), and the Pennsylvania AG (2024, $158,924 in restitution to 1,309 Pennsylvania consumers). DC regulators found effective APRs above 500% on typical SoLo loans. Availability in New York has been restricted and shifting; verify before signing up.

Where Tip-Based Apps Stand Legally in New York

This is the genuinely unsettled piece of the picture. In December 2025, the CFPB formally withdrew its 2024 proposed interpretive rule that would have pulled earned wage access products under the Truth in Lending Act. Separately, the CFPB's May 2024 lawsuit against SoLo Funds was voluntarily dismissed in February 2025. With federal enforcement pulling back, state caps and state AGs are doing most of the work here.

New York has not publicly taken the same line California took with its 2025 EWA registration rule, but the mechanics of GOL 5-501 are already strict. If a "tip" plus an "expedite fee" on a small advance implies an annualized cost above 16%, a New York civil usury argument is at least plausible, and above 25% it becomes a criminal-usury question. That risk is why most tip-based products operate cautiously in New York and why some cap optional tips here that they do not cap in other states.

What to Do if You Were Charged Above the Cap

If a loan app charged you interest, fees, or tips that in combination exceed what New York allows, you have real tools:

- File a complaint with NYDFS at dfs.ny.gov/complaints. Attach your loan agreement, billing statements, and the app's state-specific disclosure screen if you screenshotted it.

- File with the NY Attorney General at ag.ny.gov, especially if the app made misleading statements about legality or its New York license.

- NYC residents: Add a parallel complaint to NYC DCWP at nyc.gov/dcwp if debt-collection conduct is involved.

- Consider legal aid. Legal Services NYC, New York Legal Assistance Group, and the Legal Aid Society all handle consumer debt cases and can advise on GOL 5-511's voiding provisions.

Your Next Steps if You're Borrowing in New York

Before you sign anything inside a loan app from a New York IP, do three things. Check the app's state-availability disclosure (usually in the footer or the final loan-agreement screen, not the marketing page). Verify the lender's New York Licensed Lender status in the NYDFS licensee search. Calculate your full cost including any "optional" tip or expedite fee, annualized, and compare it to 16% and 25%. If the math is above 25%, stop. You have a stronger hand than you think.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 What is the maximum legal APR on a loan app in New York?

For non-bank consumer loans to individuals under $250,000, New York sets a 16% civil usury cap under General Obligations Law 5-501 and a 25% criminal usury cap under Penal Law 190.40. Loans above 25% are a Class E felony. Licensed banks and certain federally preempted lenders operate under different frameworks, but most app-based products are bound by these ceilings.

02 Why do so many loan apps say they cannot lend in New York?

Most national loan apps price above New York's 25% criminal usury ceiling. Combined with NYDFS's 2020 "true lender" position, which treats bank-partner fintechs as the real lender for state-law purposes, these apps either restructure their New York product or geofence the state entirely. It is regulation working as designed, not a technical glitch.

03 Is EarnIn legal in New York?

EarnIn's base earned wage access product operates in New York for users whose employers are supported. The company's fee structure relies on optional tips and expedite charges rather than mandatory interest. That model has drawn regulatory scrutiny nationally because the implied APR can be high, but New York has not taken a formal action against it as of publication.

04 How do I file a loan-app complaint in New York?

File online with the New York State Department of Financial Services at dfs.ny.gov/complaints. Include your loan agreement, payment records, and screenshots of the app's disclosure screens. NYC residents should also file with the Department of Consumer and Worker Protection, and any borrower can file separately with the New York Attorney General's consumer frauds bureau.

05 Can I void a usurious loan in New York?

Under General Obligations Law 5-511, a civilly usurious loan made by a non-bank lender can be declared void, potentially eliminating the obligation to repay interest and in some cases principal. The specifics depend on the lender's license status and the type of loan. Consult a consumer-rights attorney or legal aid before stopping payments; voiding is not automatic.

Related articles

Loan Apps in California: What the 36% APR Cap Actually Means for Your Next Download

Loan Apps in Texas: How the 10% Usury Cap and the CAB Model Actually Set Your APR