Here is the honest answer up front: very few app-based personal loan lenders accept co-signers. A handful accept co-borrowers (which is a different legal structure, more on that in a minute). The popular names you see on "best loans with a cosigner" listicles (Upstart, OppLoans, LendingPoint, MoneyLion) almost never accept a second party at all. If you are searching for a loan app that lets someone cosign with you, the real short list is SoFi, LightStream, LendingClub, Prosper, PenFed Credit Union, Navy Federal Credit Union, Wells Fargo, and Discover, and even those accept co-borrowers, not traditional cosigners.

If you are the person being asked to cosign, read this whole article before you sign anything. Cosigning is a legal commitment that lives on your credit report, inflates your debt-to-income ratio, and can block your own future mortgage or auto loan. That is not a scare tactic. It is on the FTC's required Notice to Cosigner, which is the federal disclosure you will be handed right before you sign.

Co-Signer vs. Co-Borrower: The Distinction That Matters

This is the point most articles skip, and it is the reason so many readers end up confused at the application screen. The two roles are not the same.

A co-signer (the CFPB's working definition) promises to pay the loan if the primary borrower does not. The co-signer does not receive any of the loan money. They do not share ownership of whatever the loan bought. They are pure backup, legally on the hook for 100% of the debt from day one, and the loan shows up on their credit report the same day it funds.

A co-borrower (also called a joint applicant) is a second primary borrower. They apply together with you, share the loan proceeds, share ownership, and share liability. Both credit reports are pulled. Both incomes count toward approval. Both parties are equally responsible for payments, and a late payment hits both credit files the same way.

Most app-based lenders that allow a second party use the co-borrower structure. The word "cosigner" gets thrown around loosely in marketing copy, but when you read the fine print, it is almost always a co-borrower relationship. That matters because co-borrowers usually have to share a household, share a purpose for the loan, and in most cases, share the same address on the application.

Which Loan Apps Actually Accept a Second Party

This list reflects each lender's published policy as of the date this piece was written. Policies shift, so confirm with the app's help center before you apply.

| Loan app | Co-signer | Co-borrower | Typical min credit | APR range |

|---|---|---|---|---|

| SoFi | No | Yes (same address) | 680 | 8.99% to 25.81% |

| LightStream | No | Yes | 660 | 6.94% to 25.29% |

| LendingClub | No | Yes | 600 | 8.98% to 35.99% |

| Prosper | No | Yes | 600 | 8.99% to 35.99% |

| PenFed Credit Union | Yes | Yes | 580 | 8.99% to 17.99% |

| Navy Federal Credit Union | Yes | Yes | Varies | 8.99% to 18.00% |

| Wells Fargo (existing customers) | No | Yes | 660 | 7.49% to 23.24% |

| Discover Personal Loans | No | Limited | 660 | 7.99% to 24.99% |

Notice that the only two lenders on this list that still accept a traditional cosigner (the backup-only structure) are credit unions: PenFed and Navy Federal. Everyone else moved to co-borrower-only years ago, mostly because co-borrower underwriting is cleaner legally and gives the lender two active parties they can contact.

Which Popular Apps Do Not Accept Cosigners (and Why People Still Think They Do)

Some of the most-searched "loans with cosigner" results are flatly wrong. Here is what the lenders actually publish:

- Upstart. No cosigners. No co-borrowers. Solo applicant only.

- Upgrade. Primary product is solo applicant only.

- Best Egg. Solo applicant.

- Happy Money. Solo applicant.

- Avant. Solo applicant.

- OppLoans. Solo applicant.

- MoneyLion, Dave, Earnin, Brigit. These are cash advance apps, not personal loan lenders. They do not have a concept of cosigners.

- Possible Finance. Solo applicant, cash-flow underwritten.

Why does the internet still tell you otherwise? Affiliate content. Many of those listicles earn a commission per application, and the easier path is to list a bunch of popular lenders with a "cosigner considered" footnote that does not match the lender's real policy. When the app rejects you for not having the option to add a cosigner, the affiliate already got paid for the click. You got nothing.

If you see an article claiming Upstart accepts cosigners, close the tab (and if you're shopping with thin credit, see loan apps for bad credit under 580 FICO for solo-applicant routes). Upstart has said, in writing, for years, that they do not.

How Adding a Co-Borrower Changes Your APR

The reason to add a second party is almost always rate. A lower APR means a lower monthly payment and less total interest paid. But the APR reduction depends entirely on whose credit is stronger and by how much.

Here is a practical scenario. You have a 640 credit score and apply solo on LendingClub for a $15,000 loan over 48 months. Published APR offers in that range tend to land around 24% to 29%. Your monthly payment is roughly $475, and you pay about $7,800 in interest.

Now add a co-borrower with a 780 credit score and a stable income. Lenders generally price the loan closer to the stronger file, often landing you at 12% to 15%. Same $15,000 over 48 months at 13% is a $402 monthly payment and about $4,300 in interest. You saved $3,500.

When does adding a co-borrower not move the needle? Three scenarios:

- Both applicants have similar credit. If you are both 640, the lender prices on the average, not the better file. Savings are marginal.

- The lender is already at its floor rate. If the best published APR is 7.99%, the loan is not going below that no matter how perfect the co-borrower is.

- The co-borrower has high existing debt. Their DTI (debt-to-income ratio) may actually hurt your application even with a high credit score.

What Co-Signing Does to the Co-Signer's Credit and DTI

This is the section I wish someone had handed my parents 20 years ago.

When you cosign or co-borrow on a loan, the full loan balance shows up on your credit report (Experian walks through the bureau-side mechanics, and our own guide on whether loan apps show up on your credit report covers the broader rules). Not half. Not a percentage based on your share. The full balance. It is counted against your DTI when any future lender evaluates you for a mortgage, an auto loan, or a credit card limit increase.

Here is how that plays out. Your kid asks you to cosign on a $20,000 car loan. The car is theirs, the payments come from their account, and the loan is current. Two years later, you apply for a mortgage. The mortgage underwriter sees a $15,000 remaining balance on the car loan on your credit report. They count a $380 monthly car payment against your DTI. If that pushes your DTI over 43%, your mortgage application gets denied or downgraded, even though you have never missed a payment on anything.

The other risk is the late payment. The primary borrower misses a payment. It hits their credit report. It also hits yours. The FICO damage is the same on both files: 60 to 110 points for a 30-day late on a previously clean file. You can be the most responsible person in the country and still lose 80 FICO points because your nephew forgot to pay his loan on the 28th.

The FTC Notice to Cosigner: Read It Before You Sign

Federal law (16 CFR 444, the FTC Credit Practices Rule) requires the lender to give you a written Notice to Cosigner before you sign. The notice is short, usually one page, and it reads something like this:

You are being asked to guarantee this debt. Think carefully before you do. If the borrower doesn't pay the debt, you will have to. Be sure you can afford to pay if you have to, and that you want to accept this responsibility. You may have to pay up to the full amount of the debt if the borrower does not pay. You may also have to pay late fees or collection costs, which increase this amount. The creditor can collect this debt from you without first trying to collect from the borrower. The creditor can use the same collection methods against you that can be used against the borrower, such as suing you, garnishing your wages, etc. If this debt is ever in default, that fact may become a part of your credit record.

If the lender does not give you this notice before the closing documents, stop. They are required to, by federal rule. If they did not produce it, you can file a complaint with the CFPB at consumerfinance.gov/complaint.

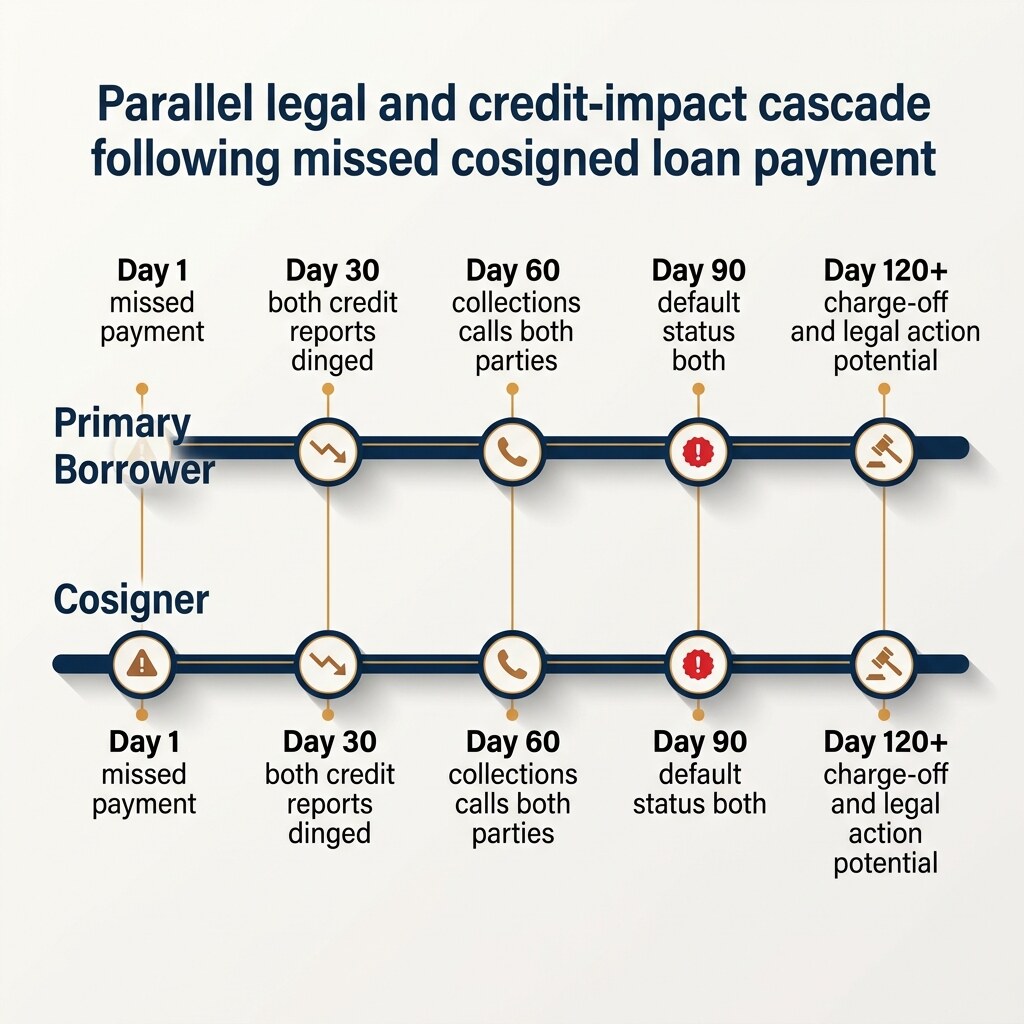

Default: What Happens to Each Party

Let's run the worst case to completion, so nobody is surprised by it.

- Day 1 to 30. The primary borrower misses a payment. The lender calls both parties. The late fee hits.

- Day 30. The late payment is reported to all three credit bureaus, on both files. Both FICO scores drop.

- Day 60 to 90. More late notices. More reporting. The lender may accelerate the loan, meaning the full balance becomes due.

- Day 120 to 180. The account charges off. It goes to collections. The collection agency can call both parties, and in most states, sue either or both.

- Post-judgment. In states that allow it, the creditor can garnish wages, file a lien on property, or levy a bank account of either party. They do not have to go after the primary borrower first.

That last point is the one people miss. Cosigners often think, "They'll try to collect from him first, then come to me." In most states, that is not how the law works. The creditor can pursue whichever party is easier to collect from, which is usually the one with a steady job, a house, and a bank account. The cosigner.

Cosigner Release: Does It Exist?

A cosigner release is a provision in the loan agreement that lets the cosigner be removed from the loan after the primary borrower hits certain milestones (usually 24 to 48 consecutive on-time payments plus a credit review on the primary borrower).

On personal loan apps, cosigner release provisions are rare. SoFi does not offer one on personal loans. LightStream does not. LendingClub and Prosper do not. Credit unions occasionally offer release on specific products, but you have to ask before signing. Assume cosigner release does not exist unless it is in writing.

If you cosign a personal loan and want out before the loan is paid, your two real options are: (1) the primary borrower refinances into their own name, which requires their credit to have improved enough to qualify alone, or (2) you pay off the loan yourself. There is usually no third option.

Alternatives When Co-Signing Is Not on the Table

If you are the borrower and no app will accept a cosigner, or if the person you were going to ask just said no, there are real alternatives that do not require a second signature:

- Credit-builder loan. Self, MoneyLion Credit Builder Plus, Kikoff, or Brigit Credit Builder. Six to twelve months of on-time payments can add 30 to 80 FICO points to a thin file. Then reapply solo.

- Secured credit card. Discover it Secured, Capital One Platinum Secured, or your local credit union. Put down $200 to $500 as collateral, use the card, pay it off monthly. Same credit-building effect.

- Authorized user status. Get added to a family member's old, well-managed credit card. The full tradeline can appear on your credit report, protected by the Equal Credit Opportunity Act, without either of you being liable for the other's debt.

- Credit union Payday Alternative Loan (PAL). Federally capped at 28% APR, available at most federal credit unions after 30 days of membership, up to $2,000.

- CDFI personal loans. Community Development Financial Institutions often offer small-dollar loans with underwriting that goes beyond your FICO score.

The Bottom Line

If you want a cosigner on a loan app, your real options are PenFed and Navy Federal. Everyone else uses the co-borrower structure or does not accept a second party at all. If you are being asked to cosign, read the Notice to Cosigner, run the DTI math on your own future borrowing, and assume the worst-case default before you sign. The goal is not to scare anyone out of helping family. It is to make sure both people know what they are signing up for.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Which loan apps accept a cosigner?

Very few. PenFed Credit Union and Navy Federal Credit Union accept traditional cosigners on personal loans through their mobile apps. SoFi, LightStream, LendingClub, Prosper, and Wells Fargo accept co-borrowers (joint applicants), which is a different legal structure where both parties share the loan. Upstart, OppLoans, Best Egg, Upgrade, and Happy Money accept neither.

02 What's the difference between a cosigner and a co-borrower?

A cosigner promises to pay if the primary borrower defaults but does not receive any loan proceeds and has no ownership of what the loan buys. A co-borrower is an equal primary borrower who shares the money, the responsibility, and the credit impact from day one. Most app-based lenders that allow a second party use the co-borrower structure, not the cosigner structure.

03 Does cosigning a loan hurt your credit?

It can. The full loan balance appears on the cosigner's credit report and counts toward their debt-to-income ratio for future mortgage, auto, or credit card applications. If the primary borrower pays on time, the effect on your FICO score is usually small. If they miss a payment, your FICO score takes the same hit theirs does, typically 60 to 110 points on a previously clean file.

04 Can I be removed from a cosigned loan?

Rarely without refinancing. Most app-based personal loans do not offer a cosigner release provision. Your two real paths off the loan are (1) the primary borrower refinances the loan into their own name alone, which requires their credit to have improved enough to qualify, or (2) the loan is paid off in full. Always check the loan agreement for release terms before signing.

05 What is the FTC Notice to Cosigner?

The FTC Notice to Cosigner is a one-page federal disclosure required under 16 CFR 444 that explains the cosigner's full legal responsibility for the debt, including possible wage garnishment, liens, and credit damage if the primary borrower defaults. The lender must provide it before you sign. If you never received one, you can file a complaint with the CFPB at consumerfinance.gov.

Related articles

Do Loan Apps Show Up on Your Credit Report? A Plain-English Breakdown for 2026

Loan Apps for Bad Credit (Under 580 FICO): What Actually Approves You in 2026